Introduction to Money Management

Money management is probably the most important aspect of managing a trading account. It is something so simple that can be learned in ten minutes and certainly is one of the most important causes of losses for most traders, usually in a reduced time.

As the name suggests, Monetary Management is nothing more than a set of techniques that help us to determine the size of our position to control potential losses that may arise when the market move against us.

Due to the high leverage offered in the Forex trading, many inexperienced traders assume a higher risk than any investor should take, resulting in hardly recoverable losses.

How to calculate the position size?

It is such an important topic that I decided to write a specific article to detail in-depth on this subject, so this section will be nothing more than a summary. You can find more information in the following article:

To make it more practical, we will see the steps with an example. In this case, we will assume that we have an account with 2,000 EUR, we are trading with GBP/USD, we risk 150 euros per trade, and the stop loss in pips for every trade is 70 pips.

The steps to determine the position size would be:

- Determine the amount of money you want to risk per trade: in this case 150 euros

- Set the distance in pips of the Stop Loss to be used: in this case, 70 pips

- Calculate the value of Stop Loss in the account currency for one standard contract, in this case:

- Set the size of your position as a simple rule of three.

- If I risk 645 EUR with 1 contract (100000), how many contracts do I have to trade to risk 150 euros?

- This step is not necessary, but in a didactic way, we find that we are actually taking that risk

The expectation in money management

In this context, the expectation is a statistical concept that comes to determine whether our trading approach will yield a positive result in the medium or long term, always based on the previous results.

Keep in mind that past performance is not necessarily indicative of future results, but if we have a system with an extensive history of transactions (either in backtesting or trading in real or demo), we can get an idea of what will be our results if market conditions will not change and we trade according to the same methodology.

In calculating the mathematical expectation two main factors are taken into account:

- The percentage of winning trades versus losing trades. This factor is quite intuitive because what it tells us is that if we win more than we lose in our trades, our expectations will be higher.

- The amount of money we make when we win, against the amount of money we lose when we lose. While trading is an activity where one has a variable result (not like other activities or games), you will need to consider how much you earn and how much you lost on average to determine the likelihood of success, which after all, is what matters to us.

Mathematical expectation (ME) = (% Winning * Average earnings) – (% Loss * Average loss)

- Scalping system which risks 20 pips and normally close with a 5 pips profit and has a percentage of winning trades of 70%:

- ME = (70% * 5) – (30% * 20) = -2,5

- Trend following system which risks 100 pips and normally close with a 250 pips profit and has a percentage of winning trades of 35%:

- ME = (30% * 250) – (70% * 100) = +5

Concerning how to interpret the results, it is clear that a positive mathematical expectation indicates a winning system, whereas if negative, it will involve a loser system, but what tells us that -2.5 or the 5? The result will be given in the same units in which have been calculated, that is, in our previous example, a mathematical expectation of +5 indicates that for every trade we do, we expect to gain 5 pips on average.

We could also have calculated the mathematical expectation of the amount of money won or lost, instead of pips, and the result would tell us how much money you can expect to earn on average on every trade performed.

As can be inferred from the above examples, it is not just about having more winning trades than losing trade, but we also have to take into account the amounts won and lost on each trade.

It is very typical to find systems that always close in positive and have a hit rate of 95%, but these are systems in which the trader is not using stop loss and hopes that sooner or later the price will return to its entry-level if the market moves against. The problem with such systems is that there are times when the price does not return, or at least it does after smashing your account.

Benefit/Risk Ratio

This section relates to the second factor affecting the expectation of our system, that is, how much we earn when we win, and how much we lose when we lose.

Many authors are defending the idea that we should always seek in every trade more benefits than assumed potential losses, even indicating that a trader should seek a Profit/Loss ratio of at least 2:1 (ie, if we risk 10 then we should get a profit of 20 at least).

Usually, the result of a trade is indicated based on what we call R (Risk), that is, if we say that we have achieved in the trade an outcome of a 2,3R, it means that we have earned 2.3 times what we have risked assuming that we set a stop loss.

A very important thing to note is that the percentage of winning trades is inversely related to the risk-benefit ratio, that is, when we look benefits above the amount risked, our hit rate decreases.

This should be completely intuitive, but let’s explain a little more because it is important. Imagine that there are no transaction costs and we are fortunate to trade at mid-price, that is, there is no spread or difference between the bid/offer.

If we enter the market based on heads or tails and we put a take profit and stop loss of 20 pips, we will have a hit rate of 50% (always assuming that the market moves randomly).

However, if we set a target of 20 pips and a stop loss of 100 pips, it is normal that we win many more times than we lose, and if reversed, we would normally lose many more times than we win.

This is very typical in trend followers systems, where there is a high failure rate, but when a good trade is caught, it compensates all previous losses, because these trades can get a 15R or 20R.

It is important to understand the relationship between the percentage of winning trades and the risk-benefit ratio.

Because of this, we can make money in trading with a hit rate of only 30% (3 winning trades out of 10), if our risk/benefit ratio is greater than 2.5R.

By contrast, with a hit rate of 70% (7 winning trades out of 10)and a gain of only 0,25R per transaction, in the end, we will end up losing money in the medium term.

The following table shows the minimum percentage of winning trades we need to get to have a positive mathematical expectation. The percentages shown represent a zero or null ME.

Minimum percentage of hits based on R | |||||||||||

R | 0,15 | 0,3 | 0,5 | 0,75 | 1 | 1,5 | 2 | 2,5 | 3 | 3,5 | 4 |

%Hits | 87 | 77 | 67 | 57 | 50 | 40 | 33 | 29 | 25 | 22 | 20 |

Now, with all this, what benefit/risk ratio should I pursue?

The answer to that question is known by no one else but you, because the use of a large or small R depends on the trader psychology.and their objectives. Some people prefer to win many times although in the losing trades they end up losing a high percentage of their account, while others have no problem losing many times in a row waiting for “a great opportunity”.

I try to find returns of 2R up, but when I have several trades in a row in which I had a benefit of 1R and remain open, I always stakeout this subject because it is very frustrating to see how the already achieved benefits vanish.

The multiplier effect of the reinvestment

Usually, a trader begins to withdraw money as he gets benefits. However, if we let the account grow and grow without any money withdrawn, we can capitalize on this account at a much faster pace, as we will use the power of compound interest.

In simple terms, we just need to understand that a profit of 6% monthly will not produce a profit of 72% per year as some people would venture to say, but a 100% return per year. If we can increase this percentage, profitability will be much higher.

In other words, if we make good trading, eventually, you can earn a lot of money.

The importance of controlling losses

This is something that everyone should understand clearly, as though in small amounts could be indifferent when the losses are higher the difference can be huge.

We could summarize this point as follows: “If you lose 1% of the account you have to earn 1.01% to recover, but if you lose 50%, you need a 100% return to get back to the starting point.”

The following table shows the necessary gain to return to the starting point after a certain percentage of loss. Many authors consider that a loss of 25% begins to be at the limit of “no return”.

That is, if you were able to get a monthly return of 6%, after 10 years, 100 euros will have become 108,818 euros (100 * (1 + 108719%)), and if you start with a capital of 2,000 euros, for example, you would have accumulated 2,176,000 euros.

That said, however, we must also be realistic. The best managers fail to outperform 30% – 35% annually, and we are talking about the best. One thing is to manage an account of 2,000 euros, and another is to manage an account of several hundred thousand, where the psychological factor greatly affects our decisions.

% Loss | % Gain to recover |

1 | 1,01 |

3 | 3,09 |

5 | 5,26 |

10 | 11,1 |

15 | 17,6 |

20 | 25 |

25 | 33,3 |

30 | 42,9 |

40 | 66,7 |

50 | 100 |

60 | 150 |

70 | 233 |

80 | 400 |

90 | 900 |

100 | Bankruptcy |

Money management techniques

- Fixed percentage of capital: This technique determines that we should risk the same percentage amount over the size of our account in every trade we perform. It has several advantages, for example, when we win, we will gradually increase the size of our position, thus harnessing the power of compound interest, while when we lose, we will reduce the position size, protecting our account from further losses.

- Fixed amount per trade: In this case, we always risk the same monetary amount in each transaction. Many traders say it has the disadvantage of risk potentially a higher amount in each trade as we lose, but the truth is that it eliminates a problem present in the above method (a run of losing trades is not recovered with the same amount of winning trades) because to recover from a bad losing streak, a trader just need the same amount of winning trades to reach break-even.

- Fixed trade size (Lots) per trade: This technique involves always enter the market with the same number of lots. It is a convenient system for traders who perform many transactions, especially in scalping systems, because it is easy and quick to perform, even without orders manager.

- Optimal F: The optimal F was devised by Ralph Vince, who developed a mathematical formula to determine the optimal amount to risk on each trade for a system with positive mathematical expectation.

- Martingale: It is an aggressive money management technique that doubles your position every time you lose. We might even say that a martingale system opens new positions when a position goes against you, improving the “average price” of your position, but exponentially increasing the risk. Many systems use this money management technique, and although they can give excellent results sooner or later end up destroying an account.

The Drawdown

We call drawdown the percentage of losses of a trading account from its peak, usually derived from a series of consecutive losses.

To understand this better, let’s look at an example based on the following image:

The first DD (Drawdown) occurs on March 1, once the account reaches a balance of 15,000 euros, falling from this level to 14,000 EUR. In this case, the account loss is 6.7% in percentage terms.

The second DD occurs on June 1, where it is important to understand that it is calculated to the low reached, although the decline has occurred in form of sawtooth and therefore there was an intermediate recovery. In this case, the account goes from 18,000 EUR to 14,500 EUR, so we will have a DD of 19.45%.

It is also important to understand that the DD shouldn´t be calculated only with the closed trades, but taking into consideration the floating of the account (the positions which remain open). For example, if we plot the balance experienced by a trading account based on the results of closed trades, we will be leaving a lot of information on the table. For example, a person who is not disciplined in the establishment of Stops Loss may have closed a trade with a profit of 2%, which at one time was producing an unrealized loss of 50% of the account.

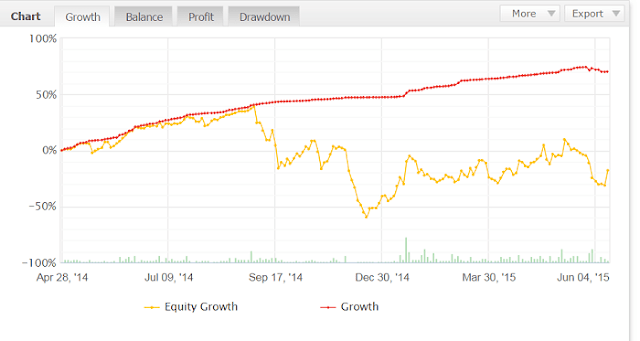

In the above graphic, there is a myfxbook account where the red line marks the balance curve, and we can see that this trader never close a trade with losses, while the yellow line plots the account balance taking into account the value of open trades at all times, to appreciate how it suffer sharp falls.

The following is a graphic of the drawdown of the same account shown previously.

I am Raúl Canessa, the founder of Forexdominion.com. As an experienced Forex trader, my passion for investing and algorithmic trading has shaped my professional journey. Over the years, I have dedicated myself to refining my skills in the financial markets, allowing me to share my knowledge and insights through my platform. I am committed to helping others understand the world of trading and develop effective strategies for success in this exciting field.