The Calmar Ratio is an indicator that is designed to measure and compare the performance of an investment portfolio or trading system.

The interesting thing about this ratio is that it summarizes how the profitability of the period has been with respect to the assumed risk.

Although it is a less known indicator than the Sharpe ratio, the Calmar ratio is currently widely used in the financial industry. It was first published in 1991 in the Futures magazine and was developed by Terry W. Young; precisely its name comes from the acronym formed from the name of the newsletter that the author sent to his clients, called CALifornia Managed Accounts Report. The Calmar ratio is defined as the ratio between the annualized profitability of the system and its maximum drawdown in absolute value.

As a risk measure, the Calmar ratio uses the maximum historical drawdown of the last 36 months (if you don’t know what the drawdown is, you can see it in this article).

As an anecdote, it should be noted that although the Calmar ratio is the most used, before the appearance of this ratio there were already very similar ones such as the Sterling ratio and the MAR ratio; even the name of the latter also comes from an acronym, the title of the Managed Account Reports newsletter founded in 1979 by Leon Rose. In any case, the formulation and the results obtained with these ratios are very similar to those of the Calmar ratio.

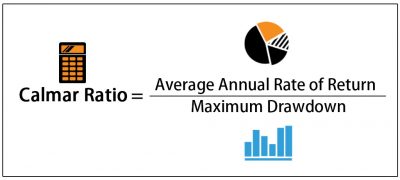

In this way, its calculation looks like this:

Calmar Ratio: Formula

The ratio is calculated as the ratio between annualized profitability and the maximum drawdown expressed in absolute value.

It is calculated on a monthly basis. To have the profitability and drawdown data, the historical data of the last 36 months are used.

Obviously, when comparing investments, the higher the Calmar ratio, the better the investment. A higher ratio indicates that the investment obtains a higher return per unit of risk.

Criticisms and comments on the Calmar ratio

Once the theoretical explanation of this ratio is finished, now it is the turn of some reflections regarding the Calmar indicator.

As we have already analyzed in the blog, there are also other ratios that measure the risk-adjusted return. We have the Sharpe ratio or the Sortino ratio, to give some examples. The difference with them is that the Calmar ratio takes the drawdown, and not volatility, as a risk measure.

Using drawdown as a risk measure has certain implications. First of all, we can say that the drawdown depends on the sequence of measurements of the past (for example if we have suffered several months with losses we will have a larger drawdown). This sequence may simply be due to bad luck and we may not find a drawdown like this in the future or, on the contrary, the biggest drawdown may wait for us in the future.

In addition, there is the fact of limiting the drawdown measurement to the last three years. If we analyze the evolution of any investment system or portfolio, we see that the more historical data we take, the greater the possibility of finding higher drawdown amounts. So why limit the data to the last 36 months? Also, what kind of analysis has led us to decide 36 months as the right figure and not 24 or 48?

The Calmar ratio is a useful metric for comparing several investment portfolios in a simple way, but in my opinion it is not good to judge a trading system solely by one ratio. It is necessary to take a more complete perspective and examine several metrics in the evaluation.

I am Raúl Canessa, the founder of Forexdominion.com. As an experienced Forex trader, my passion for investing and algorithmic trading has shaped my professional journey. Over the years, I have dedicated myself to refining my skills in the financial markets, allowing me to share my knowledge and insights through my platform. I am committed to helping others understand the world of trading and develop effective strategies for success in this exciting field.