The COVID-19 pandemic is also having dire consequences for the economy. One of the most notable effects in a large increase in public and private debt.

The world was still resentful of the great recession of 2008 when the Coronavirus health crisis erupted. With the virus spreading massively and many economies still paralyzed, states are coming to the rescue of the economy. For this, large economic stimulus programs are required, which, among other measures, include tax cuts, tax exemptions and loans on favorable terms.

Trying to avoid the fall of strategic companies, to support small entrepreneurs and to avoid a fall in the income of the most affected workers, the governments issue debt to obtain the necessary financing.

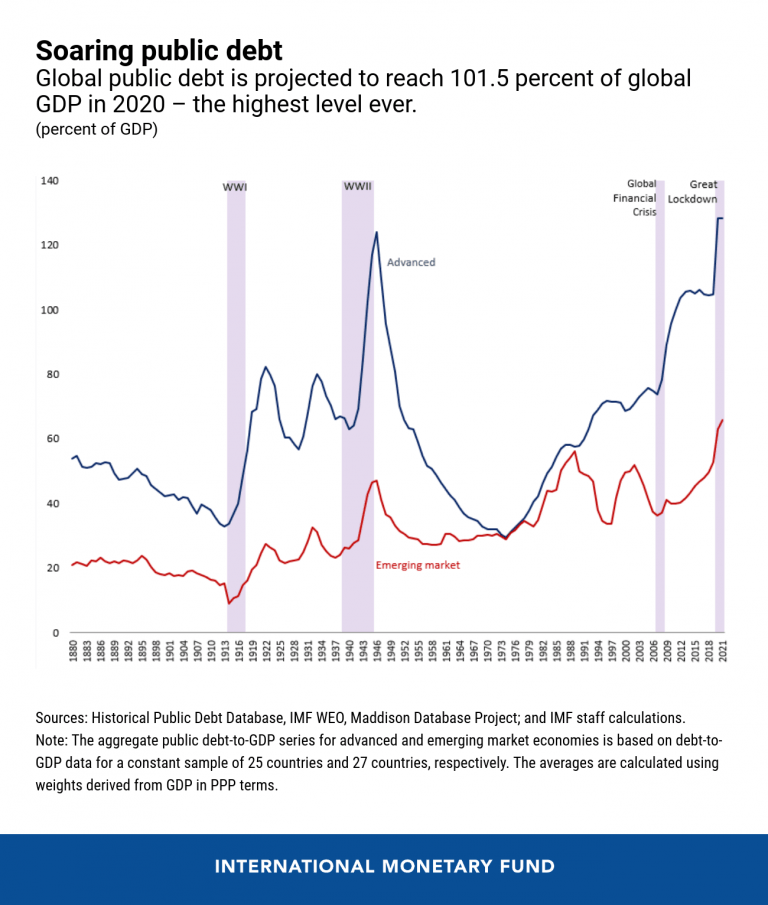

That public and private debt is increasing and will increase is a fact. Just take a look at the forecasts of the Institute of International Finance, which anticipates that public and private debt will increase from 255 to 325 trillion dollars by the year 2025. In fact, in the most developed countries, public debt will be at 130 % of gross domestic product (GDP) and in the United States it could exceed 140% of GDP. This is where many may wonder if it is possible to survive with such a high level of debt.

Debt in Europe

It is precisely in Europe that low interest rates are being maintained for governments to bear a high level of debt.

However, there are factors unrelated to economic variables that can also influence countries’ ability to face debt. Thus, in the most favorable scenario, if the pandemic evolves favorably, economic activity is restored and strong economic growth is achieved and such strong austerity measures should not be imposed. On the contrary, if a sharp increase in coronaviruses cases occurs in the worst case, countries like Italy, with a public debt that exceeds 134% of GDP, would have real problems. Investors would try to get rid of Italian bonds, which would lead us to a scenario very similar to that of the public debt crisis that took place between 2011 and 2012.

However, there are differences with the previous crisis. The reason is that the European Central Bank (ECB), with Christine Lagarde at the helm, is ready to come to the aid of the countries most affected by the pandemic and fight speculation. In this sense, the ECB contributes through debt purchase programs and converts debt to longer terms.

Latin America

The situation in Latin America is especially complicated. Its level of public debt is higher than that of the 2008 crisis and, to make matters worse, its fiscal deficits considerably limit the options of governments.

All this complicates the possibilities of obtaining financing, especially for the Latin American countries with the highest indebtedness. With worse credit scores, it will be difficult for them to obtain much-needed financing.

Among the most indebted countries in Latin America are Argentina and Brazil. Although there are few records for Venezuela, its level of indebtedness is believed to have run wild.

In the case of Argentina, the situation was already frankly complex, because before the pandemic, the country had assumed that it would not be able to pay the debt. The situation in Brazil is striking, since its level of debt is behind only Argentina

Much of Latin America maintains its debts in US dollars. Along these lines, the appreciation of the dollar and the depreciation of Latin American currencies have contributed to aggravating the situation of fiscal debt in the area.

Fiscal sustainability

There are those who defend that the accumulation of debt can end up being lethal for the economy and hinder economic growth. However, there have been experiences like those of Japan, with public debt exceeding 230% of GDP and Italy, which for a long time has maintained levels of public debt that exceed 90% of GDP. Thus, the key to living with such high levels of public debt lies in the so-called fiscal sustainability. In other words, it is about being able to face fiscal expenses with sufficient fiscal income without incurring serious deficit problems that lead to public debt problems.

However, it seems difficult to achieve this balance or sustainability. The damage caused to the economy must be contained, workers and companies must be protected and the economy must be relaunched towards solid growth.

Only with strong economic growth and increasing public income can the high level of indebtedness be reduced. The problem lies in the threat of a recurrence of the pandemic, which could destroy hopes of a strong and rapid recovery.

I am Raúl Canessa, the founder of Forexdominion.com. As an experienced Forex trader, my passion for investing and algorithmic trading has shaped my professional journey. Over the years, I have dedicated myself to refining my skills in the financial markets, allowing me to share my knowledge and insights through my platform. I am committed to helping others understand the world of trading and develop effective strategies for success in this exciting field.