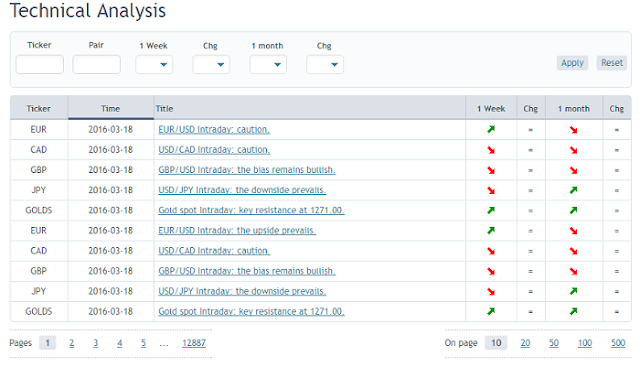

The Forex and CFD broker RoboForex (a company regulated by CySEC and IFSC) provides its clients with technical analysis updates and trading signals on currencies, gold and crude oil which can help the trader to take advantage of market opportunities.

The technical analysis and signals are supplied by Trading Central, a leading independent company specialized in technical analysis of financial markets, whose services are used by 38 of the world’s 50 leading banks as a second opinion in addition to their own in-house market analysis. The technical analysis reports from Trading Central cover many asset classes such as Forex, Commodities and Market Indices. Traders can also benefit from a wide range of reports based on a variety of technical indicators, covering multiple time frames that are ideal for short, medium and long-term traders.

Also, the clients of this broker have access to updated market news from Dow Jones.